The global cookies industry is undergoing a steady but strategically important transformation. Once viewed as a simple packaged snack category, cookies have now become a high-value segment driven by premiumization, health-conscious consumption, and rapid flavor innovation. As consumer preferences diversify across regions, manufacturers are adapting faster product cycles and more targeted offerings to stay relevant in a competitive environment.

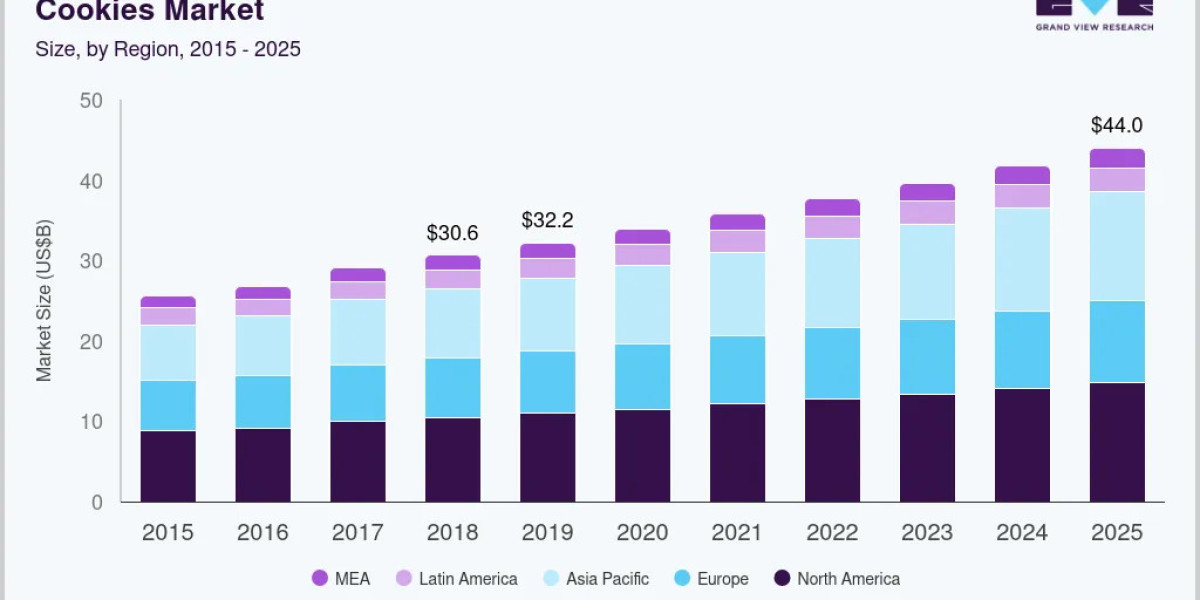

The global cookies market size is estimated to reach USD 54.9 billion by 2030, expanding at a CAGR of 4.7% from 2024 to 2030. This consistent growth reflects the category’s strong position as one of the most consumed snack formats worldwide. Cookies continue to benefit from urban lifestyles, on-the-go consumption habits, and the rising demand for indulgent yet convenient food options.

At the same time, brand competition is intensifying. The idea of a “best cookies brand” is no longer defined purely by taste or shelf presence. Instead, it is increasingly shaped by innovation, health positioning, packaging appeal, and digital visibility. This shift is pushing companies to rethink traditional product strategies and invest in differentiated value propositions.

Changing consumption patterns and product innovation

One of the most notable shifts in the cookies market is the growing demand for variety and experimentation. Consumers are no longer satisfied with standard flavors and formats. Instead, they are actively seeking premium, artisanal, and globally inspired cookie experiences. This includes ingredients like salted caramel, matcha, pistachio, and hybrid dessert formats that combine cookies with cakes, creams, or fillings.

Social media influence has also accelerated product discovery and demand cycles. Viral food trends, particularly in markets like Asia, are creating short but intense spikes in consumption for new cookie formats. As a result, product lifecycles are becoming shorter, forcing manufacturers to innovate continuously rather than rely on long-term product stability.

In parallel, health-oriented demand is reshaping formulation strategies. Sugar reduction, gluten-free alternatives, and protein-enriched cookies are gaining traction as consumers attempt to balance indulgence with wellness. This dual demand for taste and functionality is redefining how new products are developed and positioned.

Market scale, growth outlook, and industry direction

The cookies segment is expected to maintain stable global expansion through 2030, supported by consistent demand across both developed and emerging markets. Cookies remain one of the most sought-after snack categories due to their affordability, portability, and strong emotional connection with consumers.

Emerging economies are playing a particularly important role in volume growth. Rising disposable incomes, urbanization, and expanding retail infrastructure are increasing packaged snack penetration. Meanwhile, developed markets are driving value growth through premium offerings and specialty products.

Packaging innovation and sustainability are also becoming central to competitive strategy. Consumers are increasingly sensitive to environmental impact, pushing brands to adopt recyclable materials and reduce plastic usage. This shift is not just regulatory but also reputational, influencing purchase decisions at the point of sale.

The market is also seeing increased consolidation and competition among global and regional players, each competing for shelf space, brand recall, and digital engagement.

Key cookies companies shaping global competition

The competitive structure of the cookies industry is defined by a mix of multinational FMCG leaders and strong regional players. These companies collectively control significant market share and play a major role in setting pricing, innovation, and distribution trends:

- Nestlé S.A.

- Mondelez International, Inc.

- United Biscuits (UK) Limited Co.

- Grupo Bimbo

- Kellogg’s

- Campbell Soup Company

- Britannia Industries Limited

- Ferrero Group

- ITC Limited

- General Mills, Inc.

These organizations continue to expand through product diversification, acquisitions, and localized flavor strategies. Their focus is increasingly shifting toward premium offerings, limited-edition launches, and health-forward product lines. In many cases, regional leaders are also challenging global brands by offering culturally adapted products at competitive pricing.

Strategic outlook: where growth is heading

The future of the cookies industry will be shaped by three core forces: innovation speed, health alignment, and brand differentiation. Companies that can consistently launch new products while maintaining quality and cost efficiency will be better positioned to capture market share.

Digital channels are also becoming critical for brand visibility and consumer engagement. Online-first product launches, influencer-driven campaigns, and data-led marketing strategies are helping brands identify micro-trends faster and respond with agility.

Ultimately, the definition of the “best cookies brand” is shifting from mass recognition to relevance. Brands that understand evolving consumer expectations—balancing indulgence, wellness, and experience—will lead the next phase of growth in the global cookies market.